We don’t mean to speak a foreign language, but any profession has its jargon. Here are some examples of common appraiser jargon and their meanings:

Adjustment. When comparable properties have been identified, the appraiser makes adjustments to the Sales Price of each of the comparables to bring them into equivalency with the subject property, accounting for differences in location, construction quality, living area, acreage, frontage, amenities and the like. This is where the professional expertise of an appraiser is most valuable.

Comparable or “Comp”. Properties like the subject property nearby which have sold recently, used as a basis to determine the fair market value of the subject property.

Drive-by. An appraisal that is limited to an exterior-only examination of the Subject to make a determination that the property is actually there and has no obvious defects or damage visible from the outside. Fannie Mae’s form for this type of appraisal is its 2055, so you may hear a drive-by referred to as a “2055.” Click here for a PDF example.

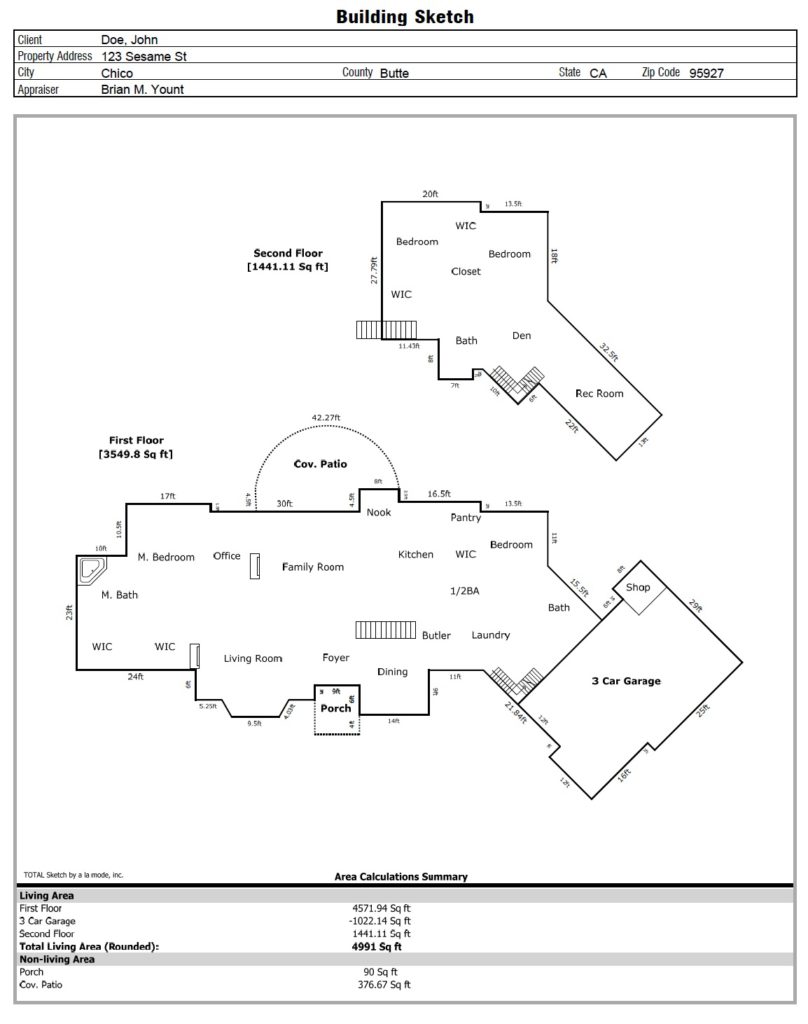

GLA. “Gross Living Area,” the square footage of all livable, above grade floor space, including stairways and closet space. GLA is often determined using exterior wall measurements.

Market value. The appraiser’s opinion of value as writen in the appraisal report should reflect the fair market value of the property — what a willing & informed buyer would pay a willing seller in an arm’s-length transaction. A more thorough definition is here.

MLS. A Multiple Listing Service is a proprietary listing of all properties on the market in a given area and their listing prices, as well as a record of all recent closed sales and their sales prices. Although most commonly used by real estate agents, appraisers used these databases to aid in comparable selection and adjustment research.

Obsolescence. The value of assets diminishes as their capabilities degrade or more desirable alternatives are developed. Functional obsolescence is the presence or absence of a feature which renders the property undesirable. Obsolescence can also occur because the surrounding area changes, making a feature of the property less desirable.

Subject. Short for the property being appraised — the “subject property.”

Useful life. The time during which a property can provide benefits to its owner.

URAR. Short for Uniform Residential Appraisal Report, Fannie Mae form 1004, it is the form most lenders require if they need a full appraisal (that is, with walk-through inspection). Click here for a PDF example.

USPAP. Short for Uniform Standards of Professional Appraisal Practice, USPAP promotes standards and professionalism in appraisal practice, and is often enacted into law in a state. It is promulgated by the Appraisal Foundation, a non-governmental entity chartered by Congress to, among other things, maintain appraisal standards.